13 Julie 2026 Saamgestel deur Kobus Hartmann Opsomming -Gebruik van plantgroeireguleerders, wat natuurlike fito-hormone en…

China Market Update for South African Pecan Nut Producers Association NPC

May 11, 2026

Economic Update

- Summary: China’s official Q1 2026 GDP growth of 5.0% year-on-year was slightly above expectations and the country’s exports and industrial output remained strong despite geopolitical tensions and energy-market disruptions linked to the Iran conflict.

But the economy continues to follow the “two-speed” pattern that emerged in the post-Covid, post-property-correction period: growth is driven mainly by exports, advanced manufacturing, and state-led investment, while the domestic economy remains caught in a weak-demand loop in which modestly rising household incomes are not enough to offset weak confidence, soft labor-market conditions, property-related wealth effects, and persistent price competition across the economy.

Two factors will determine whether this weak-demand loop begins to break: first, whether the housing market can find a durable bottom. Some signs of stabilization have appeared in China’s largest and wealthiest cities, but it remains unclear whether these mark a sustained recovery. Second, whether China can achieve a more meaningful rebalancing away from export- and investment-led growth toward broad-based domestic consumption.

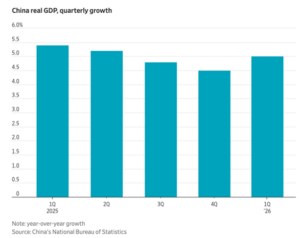

- GDP, Trade and Output: China’s Q1 2026 GDP grew 5.0% year-on-year, accelerating from 4.5% in Q4 2025 and beating an economist consensus of 4.8%. However, part of the strong GDP growth may have been related to a downward adjustment of last year’s first-half growth by the National Bureau of Statistics, which made this year’s results look better by comparison.

The composition of growth remains unbalanced, with exports and industrial activity continuing to account for much of the increase in GDP during early 2026. China’s exports rose 14.1% year-on-year in April to a record monthly high. The country posted a trade surplus of US$84.8 billion in April, leaving it on track for a third consecutive year of roughly trillion-dollar trade surpluses. Despite the large trade surplus, imports also hit a new record monthly high in April.

Industrial profits rose 15.5% year-on-year in the first quarter, though the gains appear to have been concentrated in export-oriented, equipment, and high-tech manufacturing sectors rather than reflecting a broad-based improvement across the economy. Infrastructure investment also remained an important component of growth, rising 8.9% year-on-year in Q1 on continued spending in areas such as railways and power grids.

Official messaging increasingly presents stronger domestic demand as a long-term strategic priority. In the near term, however, recent Politburo signaling suggests little urgency around monetary easing, which may also imply limited appetite for expanding consumer-focused subsidies or other forms of direct demand stimulus beyond what has already been allocated for 2026.

- Consumption Power, Consumer Confidence and Prices: Inflation began to tick up in early 2026, with the consumer price index rising 1.2% year-on-year in April, above economists’ expectations of 0.9%. However, the increase appears to have been driven more by higher input and energy costs — particularly those linked to the Iran conflict — than by stronger household demand.

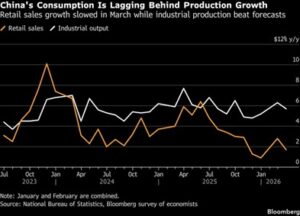

Domestic consumption growth continues to lag behind the rest of the economy. Total retail sales rose 2.4% year-on-year in the first quarter, compared with GDP growth of 5.0%, highlighting the continued imbalance between industrial/export activity and household demand. March retail sales growth slowed further to 1.7% year-on-year. Consumer confidence has improved modestly from recent lows, but remains weak by historical standards.

May Day holiday data suggest that consumers are still willing to spend selectively, but remain cautious. Domestic trips rose 3.6% year-on-year and total tourism spending increased 2.9%, yet per-trip spending declined slightly from last year and remained below pre-pandemic levels. Economists cautioned that such holiday bursts have repeatedly failed to translate into a durable recovery in household consumption.

Income growth remains positive, but not especially strong. Official data show urban household salary income growth slowed to 4.2% year-on-year in the first quarter, down from 5.2% a year earlier, while urban household property income grew just 0.6%, reflecting the ongoing drag from weak real estate conditions. Unemployment ticked up across several age groups, with the rate for 16- to 24-year-olds rising to 16.9% in March from 16.3% in February, underscoring continued labor-market softness.

- Property Market: The property sector remains arguably the single largest drag on household confidence and domestic demand, although there are tentative signs of stabilization in some major cities. Bloomberg reported that some analysts at Citi, Bank of America, HSBC, and JPMorgan have become more optimistic in their outlooks, citing improving second-hand housing activity in top-tier cities and slower rates of price decline.

However, the same article emphasized that similar optimism has been misplaced before. Recovery, if it proves durable, is still expected to be uneven and concentrated first in major cities. Lower-tier cities are likely to remain under pressure for much longer due to oversupply, weak demand, soft income expectations, and demographic headwinds.

- Currency: The renminbi has strengthened against the U.S. dollar over the past year. The monthly average exchange rate moved from around 7.22 RMB per USD in May 2025 to around 6.80 RMB per USD in early May 2026, representing an appreciation of roughly 6% — the yuan’s strongest level against the dollar since early 2023.

Sources:

Bloomberg: Wall Street Dares to Ask If China’s Property Turnaround Is Close

Bloomberg: Chinese consumers open wallets as malaise lifted during holidays

CNBC: China industrial profits jump 15.8% in March, fueled by AI and chip boom despite oil shock risks

CNBC: China inflation beat estimates in April as Iran war drives producer prices to three-year highs

China Leadership Monitor: China’s Economic Involution: State and Business Strategies

FRED / OECD: Consumer Opinion Surveys: Composite Consumer Confidence for China

National Bureau of Statistics of China: Retail sales, household income, youth unemployment, and consumer price index data

The Economist: Why China’s exports will keep on rising (April 25 edition)

The New York Times: China’s G.D.P. Stronger Than Expected, Led by Infrastructure Spending

The New York Times: China’s Exports and Imports Set Records in April Amid High Energy Costs

Reuters: China’s May Day overall tourism activity rises, but travellers are cautious

The Wall Street Journal: China’s Economy Starts Year on Strong Footing, but Iran Risks Loom

The Wall Street Journal: China’s Factory Activity Holds Up Despite Middle East Disruptions

The Wall Street Journal: China’s Industrial Profits Jump Despite Tighter Energy Markets

China Nuts Industry Update: January through April 2026

China’s Domestic Pecan Production

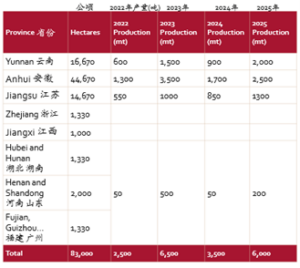

A summary of China’s pecan production was presented at the China Nuts Conference in Hefei in April. Although still at a low base, China’s pecan output is expected to continue increasing briskly in coming years as more trees enter prime bearing age, with the harvest expected to reach 8,000 to 10,000 tons in 2026. The geographic distribution is as follows:

More domestic pecan products were present at the Hefei show compared to previous years, but the quality varied widely. Industry standardization, variety improvement, per-hectare yield, and improved drying infrastructure were cited as key areas where China’s pecan industry needs to improve. China currently grows the Pawnee variety, which performs well in the market but has relatively weak disease resistance.

In January, an article appeared in a local news outlet in Jiangsu province touting cooperation between JD.com and domestic pecan growers to sell China-produced pecans directly to consumers. The article claimed (erroneously to our understanding) that imported pecans typically take six months or longer from harvest to reach Chinese consumers and therefore are not as fresh as those grown domestically. It made the further point that domestically grown pecans were more suitable for selling as a refrigerated “fresh” nut, with a high moisture content — a category that has been gaining traction in China in recent years in the form of fresh refrigerated walnuts, pine nuts, macadamias, and cashews.

China Opens Market Access to Uruguayan Pecans

China’s General Administration of Customs (GACC) announced on February 25 that Uruguayan pecans are now eligible for import into China, provided they meet the new inspection, quarantine, and sanitary requirements. The approval covers both in-shell and shelled pecans and requires registered production sources, pest-free shipments, and phytosanitary certification before export.

Source: https://mp.weixin.qq.com/s/de0J8v7qNkJlBh5CW-s4og?scene=1

Official announcement: http://www.customs.gov.cn/customs/2026-02/26/article_2026022611305625546.html

Related Posts